Introduction:

Imagine waking up on a Tuesday morning and realizing something powerful:

You don’t have to work today if you don’t want to.

Not because you won the lottery.

Not because you inherited wealth.

But because your investments quietly pay for your lifestyle.

This idea sits at the heart of the FIRE movement — Financial Independence, Retire Early. Over the last decade, FIRE has reshaped how millions of people think about money, work, and long‑term freedom.

Instead of waiting until age 65 to retire, many people are designing financial plans that allow them to achieve financial independence in their 30s, 40s, or early 50s.

But FIRE isn’t simply about quitting your job early. At its core, it’s about gaining control over your time and financial future.

Some people retire early.

Others change careers, start businesses, or work part‑time.

The key difference?

Work becomes optional rather than necessary.

In this comprehensive guide, you’ll learn:

- What FIRE really means

- How financial independence works

- The math behind the famous 4% rule

- The different types of FIRE strategies

- Whether FIRE is realistic for average earners

- How you can start your own FIRE journey

Let’s break it down.

What Is FIRE? (Financial Independence, Retire Early)

FIRE stands for Financial Independence, Retire Early.

It is a financial strategy where individuals save and invest aggressively so their investment income can eventually cover their living expenses.

When that happens, you reach financial independence.

At that point:

- You no longer depend on a paycheck

- Your investments fund your lifestyle

- You gain the freedom to work by choice

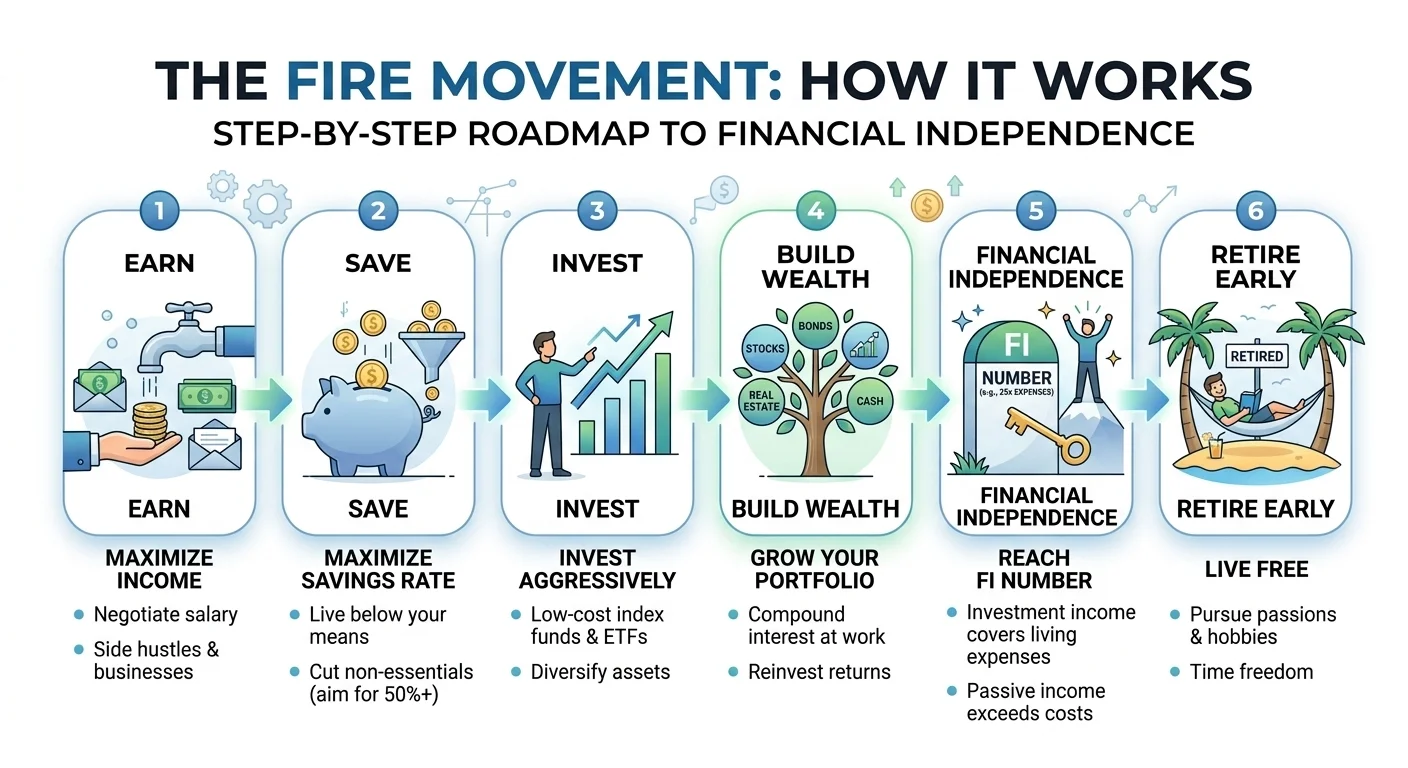

The basic formula behind FIRE is surprisingly simple:

Earn → Save aggressively → Invest consistently → Build wealth → Achieve financial independence

While traditional retirement planning assumes you will work for 40+ years, FIRE followers aim to shorten that timeline significantly.

Many pursue financial independence within 10–25 years depending on their savings rate and investment strategy.

What Does Financial Independence Really Mean?

Financial independence happens when your passive income exceeds your annual expenses.

Passive income can come from several sources:

- Stock market investments

- Index funds and ETFs

- Dividend income

- Real estate rental income

- Business income

- Retirement accounts

Once these income streams reliably cover your living costs, employment becomes optional.

This doesn’t necessarily mean you stop working forever.

Many people continue working because they:

- enjoy their careers

- want additional income

- pursue passion projects

- build businesses or creative work

But the critical difference is financial freedom.

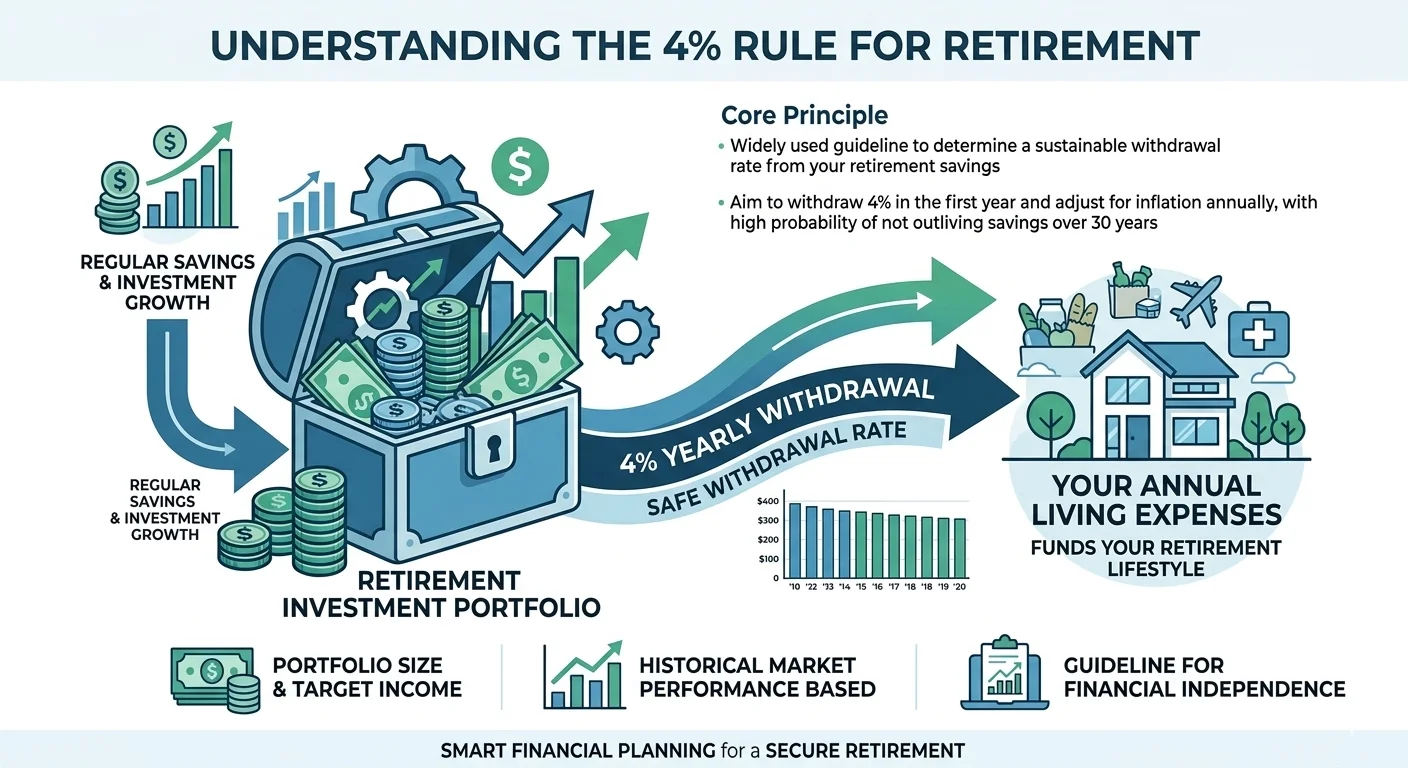

The Math Behind FIRE: Understanding the 4% Rule

One of the most important concepts in FIRE planning is the 4% rule.

This rule originates from research known as the Trinity Study, which analyzed historical market data to determine safe withdrawal rates for retirement portfolios.

The conclusion:

If retirees withdraw 4% of their investment portfolio per year (adjusted for inflation), their money historically lasted at least 30 years in most scenarios.

Simple Example

If your annual expenses are:

$40,000 per year

Your FIRE number would be:

$40,000 ÷ 0.04 = $1,000,000

So a $1 million portfolio could theoretically support $40,000 per year in withdrawals.

The FIRE Number Formula

Most FIRE calculations use a simplified formula:

FIRE Number = Annual Expenses × 25

Example:

| Annual Spending | FIRE Number |

| $30,000 | $750,000 |

| $50,000 | $1,250,000 |

| $80,000 | $2,000,000 |

Many early retirees prefer a 3–3.5% withdrawal rate for additional safety, especially if they expect retirement to last 40–50 years.

How the FIRE Strategy Works

Achieving FIRE usually involves three core financial habits.

1. Increase Your Savings Rate

The typical household saves around 5–10% of income.

People pursuing FIRE often save 30–70% of their income.

The higher your savings rate:

- the faster your investment portfolio grows

- the sooner you reach financial independence

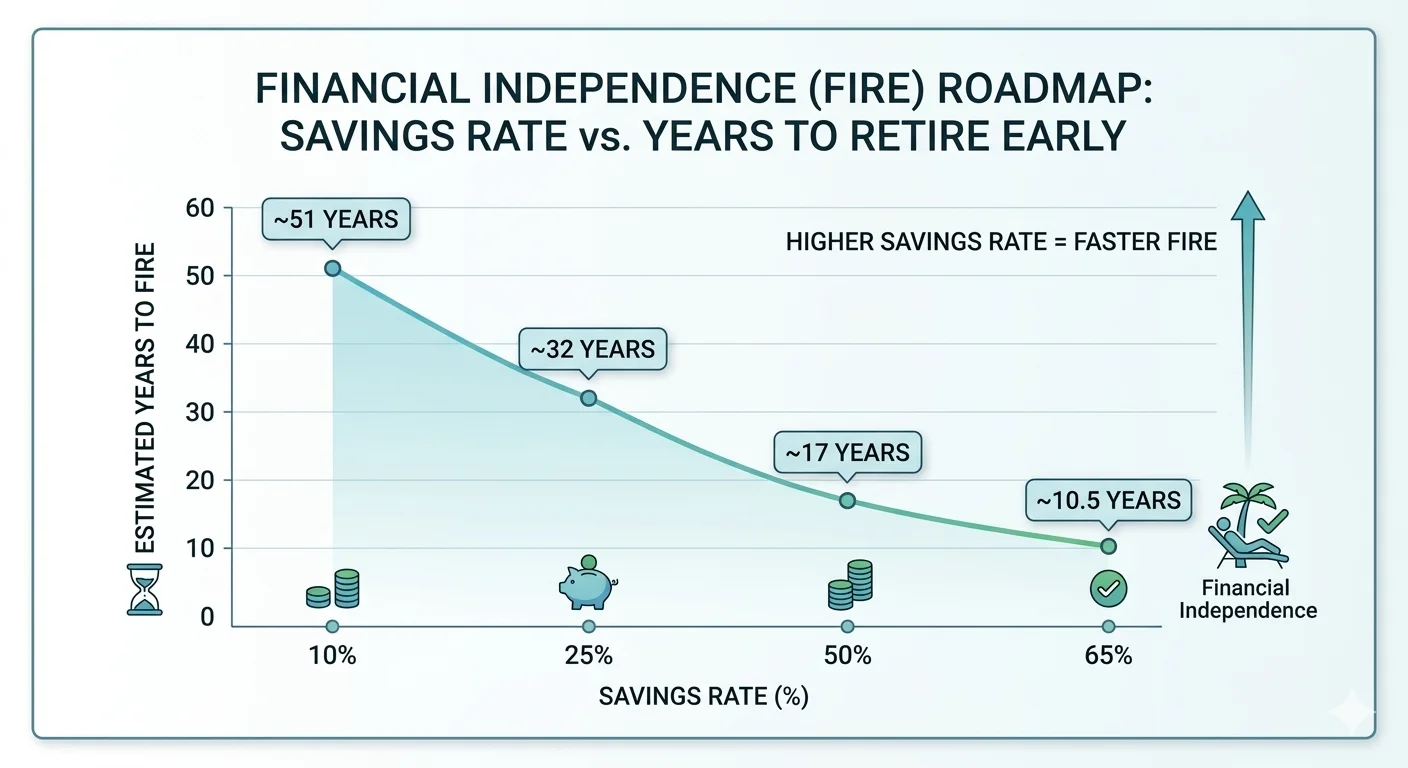

Here’s how savings rates impact timelines:

| Savings Rate | Estimated Time to FIRE |

| 10% | 45+ years |

| 25% | ~32 years |

| 50% | ~17 years |

| 65% | ~10–12 years |

This is why FIRE followers focus heavily on intentional spending and budgeting.

2. Invest for Long‑Term Growth

Saving money alone is not enough.

Your savings must be invested in assets that grow over time.

Common FIRE investments include:

- Low‑cost index funds

- Exchange‑traded funds (ETFs)

- 401(k) retirement accounts

- Roth IRAs

- Health Savings Accounts (HSAs)

- Real estate investments

Most FIRE followers prioritize broad market index funds because they provide diversification and historically strong long‑term returns.

Historically, the U.S. stock market has produced average annual returns of 7–10% before inflation.

3. Avoid Lifestyle Inflation

One of the biggest obstacles to financial independence is lifestyle inflation.

As income increases, spending often rises as well.

FIRE followers focus on intentional spending, meaning:

- cutting expenses that don’t add value

- spending freely on things that truly matter

This balance allows people to maintain happiness while increasing savings rates.

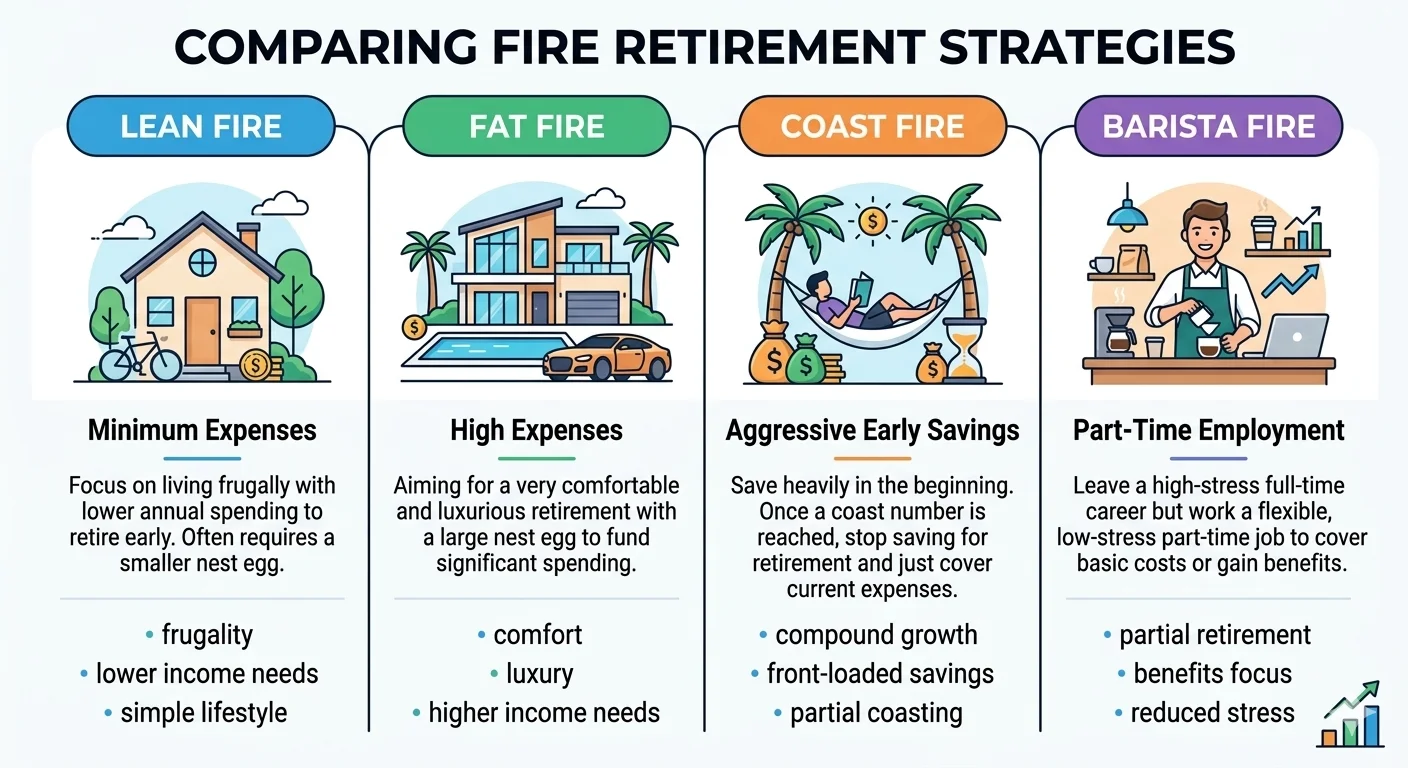

The Different Types of FIRE

Over time, several variations of FIRE have emerged to suit different lifestyles and income levels.

Lean FIRE

Lean FIRE focuses on minimalist living and lower expenses.

People pursuing Lean FIRE often aim to live on $30,000–$40,000 per year.

Because their spending is lower, their FIRE number is smaller.

Example:

$35,000 annual spending → $875,000 portfolio

Lean FIRE requires careful budgeting but allows earlier retirement.

Fat FIRE

Fat FIRE is the opposite approach.

Instead of reducing spending significantly, individuals pursue financial independence while maintaining a comfortable or luxurious lifestyle.

Example:

$120,000 annual spending → $3 million portfolio

Fat FIRE is more common among high‑income professionals and entrepreneurs.

Barista FIRE

Barista FIRE sits between full retirement and traditional employment.

People leave full‑time careers but work part‑time to cover some expenses.

Benefits include:

- reduced savings requirements

- access to employer health insurance

- lower financial stress

This strategy allows more freedom without needing a massive investment portfolio.

Coast FIRE

Coast FIRE is one of the fastest‑growing strategies within the FIRE movement.

Instead of saving aggressively forever, you invest heavily early in life until your portfolio can grow on its own to support retirement.

After reaching your Coast FIRE number:

- you stop saving for retirement

- you only earn enough to cover living expenses

- your investments continue compounding until retirement age

This approach is popular because it reduces long‑term financial pressure while still ensuring retirement security.

How Long Does It Take to Reach FIRE?

Your timeline depends mainly on two factors:

- Your savings rate

- Your investment returns

Someone saving 10% of income may need over 40 years to retire.

Someone saving 50% of income could reach financial independence in under 20 years.

This is why FIRE planning emphasizes saving aggressively early in life.

Even small increases in savings rates can dramatically shorten the timeline.

Is FIRE Realistic for the Average Person?

Yes — but it requires discipline and planning.

FIRE is not limited to tech workers or high‑income professionals.

Many people who achieve financial independence include:

- teachers

- engineers

- nurses

- government employees

- entrepreneurs

- freelancers

The key factor is savings rate, not just income level.

However, FIRE does require trade‑offs.

People pursuing financial independence often prioritize:

- budgeting

- smart investing

- reducing unnecessary spending

- increasing income where possible

Important Risks and Challenges of Early Retirement

While FIRE is powerful, it also comes with financial risks.

Market Volatility

Stock market fluctuations can affect investment portfolios, especially during early retirement.

Many FIRE followers keep 2–5 years of expenses in cash to protect against downturns.

Sequence of Returns Risk

If a market crash occurs during the first years of retirement while withdrawals are happening, it can significantly reduce long‑term portfolio sustainability.

Flexible withdrawal strategies help reduce this risk.

Healthcare Costs

In the United States, healthcare before Medicare eligibility at age 65 can be expensive.

Many early retirees rely on:

- ACA marketplace insurance

- health savings accounts (HSAs)

- spousal coverage

Tax Planning

Taxes can significantly affect retirement withdrawals.

Strategic planning between:

- taxable brokerage accounts

- traditional retirement accounts

- Roth accounts

can extend the life of a portfolio.

Common Myths About FIRE

Myth 1: FIRE Is Only for High Earners

Income helps, but savings rate matters more than salary.

Many people with moderate incomes achieve financial independence through consistent investing.

Myth 2: FIRE Requires Extreme Frugality

Successful FIRE followers focus on intentional spending, not deprivation.

The goal is to remove expenses that don’t improve life quality.

Myth 3: FIRE Means Never Working Again

Many people continue working after achieving financial independence.

The difference is they work because they want to, not because they must.

How to Start Your FIRE Journey

If you want to pursue financial independence, start with these practical steps.

Step 1: Track Your Spending

Understanding your expenses helps determine your financial goals.

Step 2: Calculate Your FIRE Number

Multiply your annual expenses by 25 to estimate the portfolio needed for financial independence.

Step 3: Increase Your Savings Rate

Look for ways to:

- reduce unnecessary expenses

- increase income

- automate savings

Step 4: Invest Consistently

Focus on diversified, long‑term investments like index funds and ETFs.

Consistency matters more than timing the market.

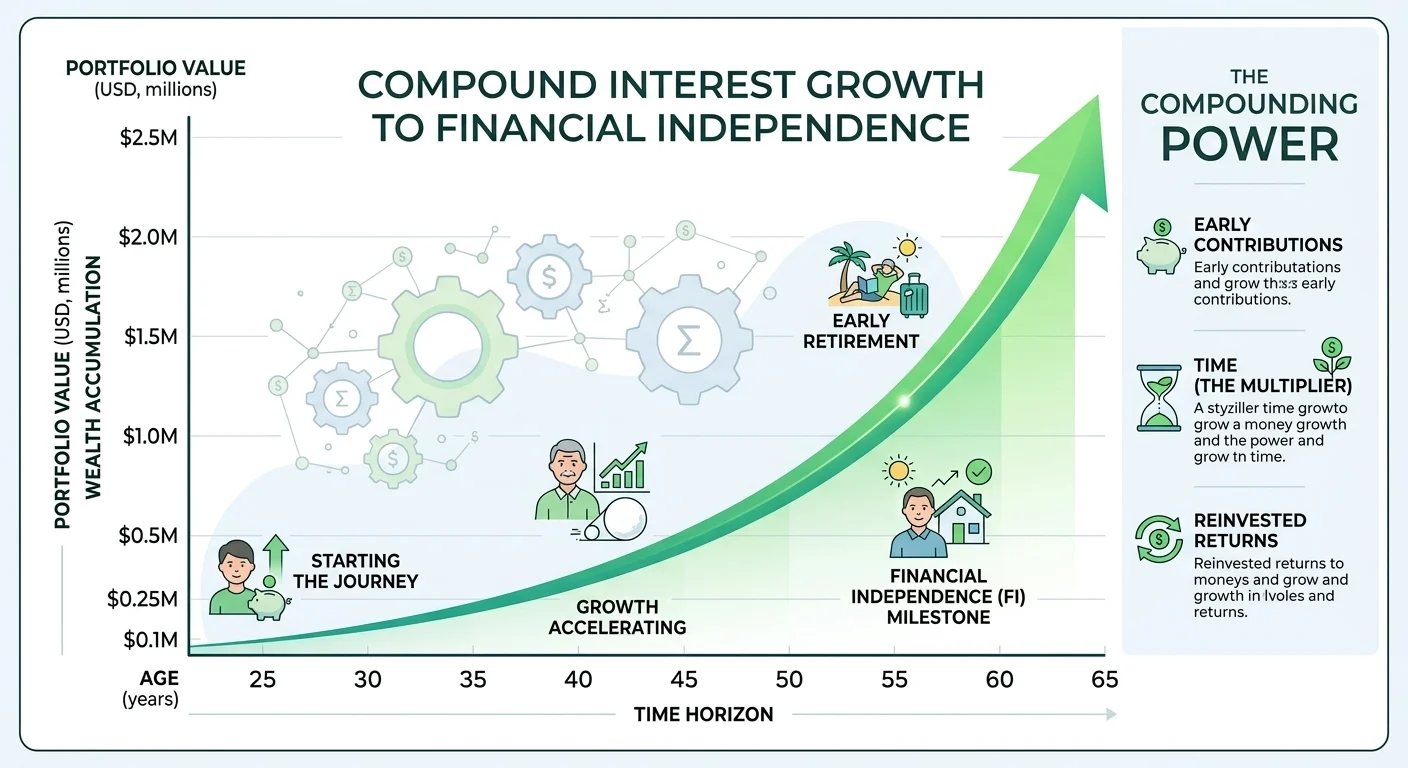

Step 5: Stay Patient

Financial independence takes time.

But compound growth becomes powerful over decades.

Frequently Asked Questions About FIRE

Final Thoughts: Why FIRE Is About Freedom, Not Just Retirement

The FIRE movement is not simply about quitting work early.

It’s about building a life where money supports your goals rather than controlling your time.

For some people, FIRE means retiring at 40.

For others, it means switching careers, starting a business, or working part‑time without financial stress.

The core philosophy remains the same:

Build investments that support your life — instead of building your life around work.

With disciplined saving, smart investing, and long‑term thinking, financial independence is possible for far more people than most imagine.