Fat FIRE is a financial independence strategy that focuses on building enough wealth to retire early while maintaining a comfortable and higher‑spending lifestyle. Early retirement doesn’t always mean extreme frugality or cutting every expense. Many people want financial independence without sacrificing comfort, travel, hobbies, or lifestyle choices. This strategy focuses on increasing income, investing consistently, and building a larger investment portfolio that can support higher annual expenses after retirement

A Fat Fire calculator helps estimate how much money you need invested to retire early while maintaining your lifestyle. Rather than focusing on reducing spending, this strategy focuses on increasing income, investing consistently, and building a large portfolio over time.

What Is Fat Fire?

Fat Fire (Financial Independence, Retire Early) is a retirement strategy that focuses on achieving financial independence with higher annual spending and a larger investment portfolio. While some FIRE strategies focus on minimal living, Fat Fire is designed for people who want to retire early without sacrificing lifestyle quality.

- Annual retirement spending: $80,000 – $200,000+

- Investment portfolio: $2 million – $5 million+

- Retirement age: 40s or 50s

The core idea of Fat Fire is simple:

Financial Independence = Investments generating enough income to cover your lifestyle.

Why Use a Fat Fire Calculator?

A Fat Fire calculator is a financial planning tool that helps estimate:

- Your target Fat Fire number

- How long it will take to reach Fat Fire

- Whether your savings rate is sufficient

- How investment returns affect your timeline

Instead of guessing your retirement number, a Fat Fire calculator allows you to model scenarios based on:

- Annual income

- Savings rate

- Investment growth

- Inflation

- Retirement spending

For example, if you plan to spend $120,000 per year in retirement, a Fat Fire calculator can quickly estimate the portfolio needed to support that lifestyle.

4 Simple Steps to Achieve Fat FIRE

Step 1: Define Your Luxury Lifestyle Budget

Start by clearly defining what “luxury” means to you. This approach goes beyond basic needs and focuses on comfort, flexibility, and premium experiences. Include high-end housing, travel, dining, healthcare, and lifestyle upgrades. A realistic estimate ensures your plan reflects your true goals, not an idealized version.

Step 2: Calculate Your Target Number

Once you know your annual expenses, multiply them by 25–30 to estimate your required investment target. A higher multiplier provides more security and supports a comfortable lifestyle without financial stress. This step turns your vision into a clear and measurable goal.

Step 3: Build High-Income and Investment Streams

Achieving this level of financial independence requires strong income growth. Focus on high-paying skills, scalable business models, or multiple income streams. At the same time, invest consistently in assets like index funds, real estate, and dividend stocks to accelerate long-term portfolio growth.

Step 4: Optimize, Track, and Scale Your Plan

Review your progress regularly and adjust your strategy based on performance. Optimize taxes, rebalance your investments, and scale your income sources over time. This is not a one-time calculation but a long-term system that evolves with your financial goals.

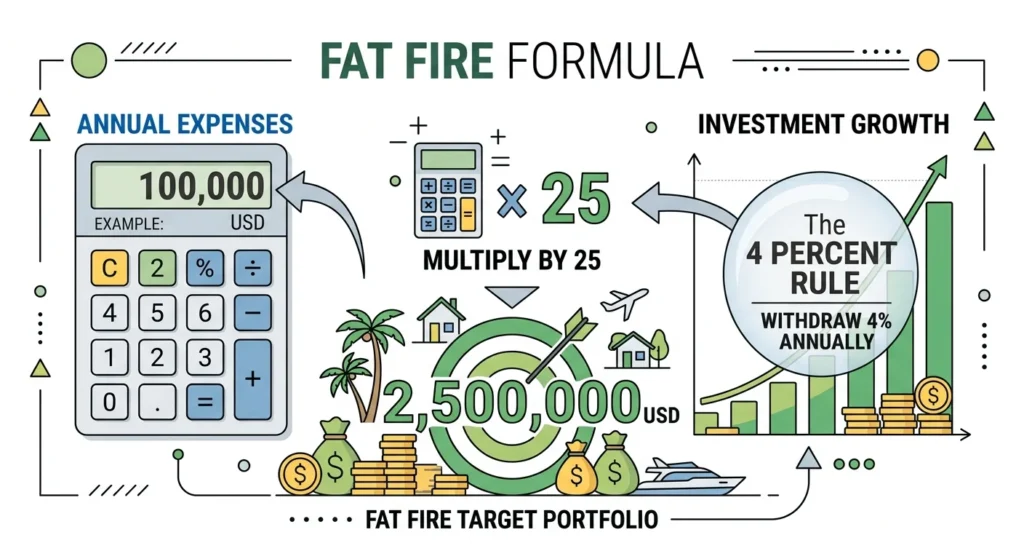

The Math Behind Fat Fire

Fat Fire uses the same formula as most financial independence strategies: the 4% withdrawal rule. This rule suggests that retirees can withdraw about 4% of their portfolio each year without running out of money for at least 30 years.

Formula

Fat Fire Number = Annual Expenses × 25

Why multiply by 25?

Because:

1 ÷ 0.04 = 25

This means you need about 25 times your annual spending invested to sustain your Fat Fire lifestyle.

Example

| Annual Spending | Portfolio Needed |

| $100,000 | $2.5 million |

| $150,000 | $3.75 million |

| $200,000 | $5 million |

| $250,000 | $6.25 million |

A Fat Fire calculator automates these calculations and includes investment growth and inflation.

What a Luxury Financial Lifestyle Really Looks Like

le Look Like?

A Fat Fire lifestyle is about financial flexibility and comfort rather than extreme wealth or reckless spending. People pursuing Fat Fire typically want to maintain a high quality of life after early retirement.

Lifestyle may include:

- Living in desirable areas

- Traveling regularly

- Dining out frequently

- Driving newer vehicles

- Strong healthcare coverage

- Owning a spacious home

The biggest difference between Lean FIRE and Fat Fire is simple:

Lean FIRE focuses on spending less, while Fat Fire focuses on earning and investing more.

Fat Fire vs Lean FIRE

Understanding the difference between Fat Fire and Lean FIRE helps clarify your financial goals.

Lean FIRE

- Annual spending: $30k–$50k

- Portfolio target: $750k–$1.25M

- Requires strict budgeting

- Faster retirement timeline

Fat Fire

- Annual spending: $80k–$200k+

- Portfolio target: $2M–$5M+

- More financial flexibility

- Longer investing timeline

Fat Fire vs Coast FIRE

Another popular strategy is Coast FIRE.

Coast FIRE:

You save aggressively early in life until your investments can grow on their own. Then you continue working to cover expenses but stop heavy investing.

Fat Fire:

Your investments fully cover your lifestyle, so you can stop working entirely.

Many people move through stages like this:

Using different calculators for each stage can help you track your financial independence progress.

FIRE Strategy Calculators for Financial Planning

Different financial independence strategies require different investment targets, which is why using the right calculator is important for planning your retirement timeline and savings goals.

A Coast FIRE calculator helps you determine how much money you need invested today so your portfolio can grow over time without additional contributions. This is useful for people who want their investments to grow while they continue working.

A Lean FIRE calculator helps estimate the minimum portfolio needed for early retirement with lower annual expenses and a more frugal lifestyle.

A Fat FIRE calculator is designed for people who want financial independence while maintaining a higher spending lifestyle and greater financial flexibility in retirement.

A Barista FIRE calculator helps calculate how much you need invested so that part‑time income and investment income together can cover your living expenses after leaving full‑time work.

Using these FIRE calculators can help you track progress, set realistic goals, and choose the financial independence strategy that best fits your lifestyle and retirement plans.

How People Actually Reach Financial Independence With a High‑Spending Retirement

Reaching financial independence with a comfortable retirement lifestyle usually requires a combination of high income, smart investing, or business ownership. Most people who achieve this level of financial freedom focus on increasing earnings, investing consistently, and building multiple income streams over time.

1. High‑Income Careers

Many early retirees come from high‑income professions that allow large investment contributions and faster portfolio growth. Common industries include technology, medicine, finance, law, consulting, and corporate leadership. Higher salaries make it easier to save and invest significant amounts each year, which accelerates the path to financial independence.

2. Business Ownership

Entrepreneurship is another common path. Many people build wealth by starting and selling businesses, owning startups with equity, investing in real estate, trading stock options, or running online businesses. A successful business exit can dramatically speed up the journey to early retirement.

3. Long‑Term Investing

Even with a high income or business success, consistent investing remains essential. Popular strategies include index fund investing, real estate investing, tax‑advantaged retirement accounts, brokerage accounts, and dividend investing. Over the long term, compound growth becomes the biggest driver of wealth and financial independence.

Advanced Strategies

Once portfolios grow large, planning becomes more advanced.

Tax Optimization

Taxes become one of the biggest expenses for Fat Fire investors. Strategies include:

- Tax‑loss harvesting

- Roth conversions

- Capital gains planning

- Asset location strategy

- Retirement withdrawal planning

Sequence of Returns Risk

Market crashes early in retirement can damage a portfolio. Many Fat Fire investors:

- Use a 3–3.5% withdrawal rate

- Keep 2–3 years of expenses in cash

- Reduce spending during market downturns

These strategies help protect a Fat Fire retirement portfolio.

How Long Does Fat Fire Take?

The timeline depends on:

- Income

- Savings rate

- Investment returns

Example

- Income: $250,000

- Savings rate: 40%

- Annual investment: $100,000

- Return: 7%

Estimated timeline:

18–25 years to reach $3–4 million

A Fat Fire calculator can give a more accurate timeline based on your numbers.

Pros and Cons

Advantages

- Higher retirement lifestyle

- More financial security

- Flexibility for unexpected expenses

- Less stress about spending

- Large financial safety margin

Disadvantages

- Requires large portfolio

- Longer working timeline

- Often requires high income

- More complex tax planning

Fat Fire trades speed for comfort and security.

Final Thoughts

Achieving financial independence while maintaining a comfortable lifestyle is possible with the right long‑term strategy. This approach focuses on increasing income, investing consistently, and building a large investment portfolio over time rather than relying on extreme frugality. A Fat Fire calculator can help estimate your target portfolio, retirement timeline, and investment strategy based on your income, savings rate, and expected returns. Once you understand your financial numbers and investment growth potential, early retirement becomes a structured and realistic goal. With disciplined investing, smart tax planning, and long‑term consistency, this strategy can help investors build lasting wealth and achieve financial freedom with lifestyle flexibility.