Lean FIRE is becoming one of the most popular early retirement strategies for people who want financial independence without needing a very high income. Instead of focusing on luxury lifestyles and high spending, this approach focuses on reducing expenses, increasing savings, and investing consistently over time. By following this method, many people are able to retire much earlier than traditional retirement timelines.

Many people believe early retirement is only possible for high earners, but that is not always true. In reality, savings rate and spending habits often matter more than income level. Someone who earns a moderate income but saves and invests consistently can reach financial independence faster than someone who earns more but spends everything. This is one of the main reasons Lean FIRE has become popular in recent years.

Another reason for the growing interest is that people are starting to value time, freedom, and flexibility more than expensive lifestyles. Many individuals want the option to stop working early, switch careers, travel, or spend more time with family. This approach provides a clear path toward that lifestyle through Lean FIRE planning.

What Is Lean FIRE?

Lean FIRE stands for Lean Financial Independence, Retire Early. It is a retirement strategy where a person keeps their living expenses relatively low so they can retire earlier with a smaller investment portfolio. Because expenses are lower, the total amount of money required for retirement is also lower, which makes early retirement more achievable through Lean FIRE.

People who follow this strategy typically focus on saving a large percentage of their income and investing it in long‑term assets such as index funds, stocks, or real estate. Over time, these investments grow and eventually generate enough income to cover living expenses. Once investment income covers expenses, a person is financially independent and no longer needs full‑time employment, which is the main goal of Lean FIRE.

Most people following this method aim for moderate annual expenses rather than luxury spending. The goal is not to live poorly but to live efficiently and intentionally while working toward Lean FIRE.

The Math Behind Early Financial Independence

This strategy is commonly based on the 4% rule. The 4% rule suggests that retirees can withdraw about 4% of their investment portfolio each year without running out of money for at least 30 years. This rule is often used when calculating Lean FIRE targets.

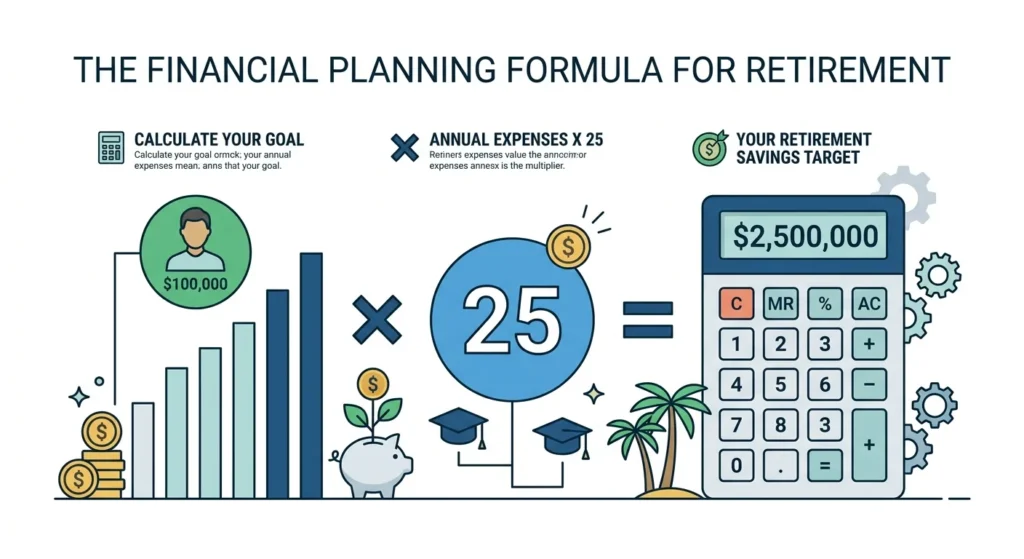

Basic Formula

Retirement Number = Annual Expenses × 25

For example, if your yearly expenses are $30,000:

$30,000 × 25 = $750,000

This means you would need approximately $750,000 invested to support that lifestyle long‑term. If your expenses are higher, your retirement number will also be higher. This formula is widely used because it provides a simple way to estimate how much money is needed for financial independence and Lean FIRE planning.

The most important factor in reaching early retirement is not just income but savings rate. A person who saves 40% to 50% of their income can reach financial independence much faster than someone who saves only 10%.

Financial Calculators for Retirement Planning

Financial calculators can help estimate how long it will take to reach financial independence and how much money needs to be invested. These tools are useful for planning and setting realistic goals for Lean FIRE.

A retirement calculator can estimate investment growth over time based on savings rate and expected returns. Some calculators also estimate how many years it will take before investment income covers expenses. Using these tools regularly can help people track progress and adjust their financial plans.

Different calculators focus on different strategies. Some calculate early retirement with low expenses, while others focus on traditional retirement planning. Using multiple calculators can provide a clearer financial picture and help people make better decisions about Lean FIRE goals.

Lifestyle and Spending Habits

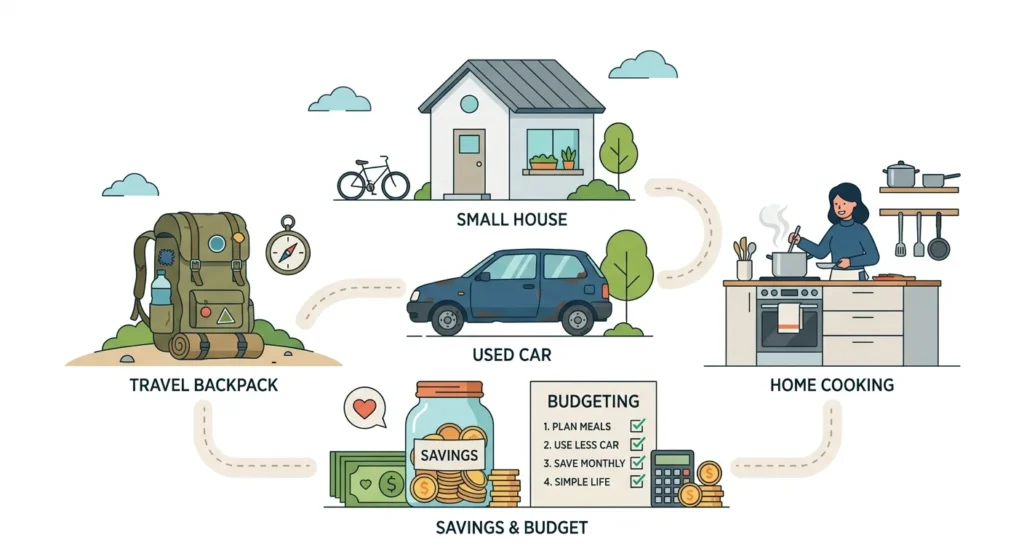

One of the biggest misconceptions is that this strategy requires extreme frugality. In reality, it focuses on intentional spending rather than cutting everything. The goal is to remove unnecessary expenses while keeping the things that provide value and happiness while moving toward Lean FIRE.

Common lifestyle choices include:

- Living in smaller or affordable homes

- Driving reliable used cars

- Cooking meals at home

- Reducing unnecessary subscriptions

- Traveling on a budget

- Buying fewer but higher‑quality products

However, people still spend money on things they care about, such as travel, hobbies, education, and health. The purpose is not to eliminate spending but to spend wisely and intentionally while following the Lean FIRE strategy.

Comparison With Other Retirement Strategies

There are several financial independence strategies, and each one focuses on a different lifestyle and retirement timeline. Some strategies focus on early retirement with higher spending, while others focus on investing early and letting investments grow over time. Traditional retirement usually involves working until age 60 or 65 and then living on retirement savings. Choosing the right strategy depends on your income, lifestyle goals, and retirement timeline.

Coast FIRE Calculator

A Coast FIRE calculator estimates how much money you need invested today so your portfolio can grow to your retirement goal over time without additional contributions. This strategy focuses on early investing and long‑term compound growth.

Barista FIRE Calculator

A Barista FIRE calculator helps calculate how much you need invested so part‑time income and investment income together can cover your living expenses. This strategy allows flexible or part‑time work instead of full retirement.

Lean FIRE Calculator

A Lean FIRE calculator estimates the investment portfolio required for early retirement with lower annual expenses and a minimalist lifestyle. This strategy focuses on saving aggressively and retiring earlier with a smaller portfolio.

Fat FIRE Calculator

A Fat FIRE calculator estimates the large investment portfolio needed to retire early while maintaining a comfortable or higher‑spending lifestyle. This strategy focuses on increasing income and building significant wealth over time.

Challenges and Risks

Although early retirement sounds appealing, there are several challenges that must be considered before choosing this path. Even with Lean FIRE, proper planning is very important.

One of the biggest challenges is healthcare costs. People who retire early must plan for medical expenses before government retirement programs begin. This can be a significant cost and must be included in financial planning.

Another challenge is market risk. Investment portfolios can fluctuate, especially during economic downturns. If the market drops early in retirement, it can reduce a portfolio faster than expected. Many people manage this risk by keeping emergency funds and reducing spending during market downturns.

Cost of living is also an important factor. Living in expensive cities makes early retirement more difficult, while living in lower‑cost areas makes it easier. Some people move to cheaper cities or countries to reduce expenses and extend their savings.

How Long Does It Take to Reach Financial Independence?

The timeline depends mainly on three factors:

- Savings rate

- Investment returns

- Annual expenses

Someone who saves a large portion of their income can reach financial independence much faster than someone who spends most of their income. In many cases, early retirement can be achieved in 10 to 20 years with consistent investing and disciplined spending using the Lean FIRE approach.

For example, a person earning $70,000 per year and saving 40% of their income could potentially reach financial independence in around 15 years depending on investment returns. Increasing income, reducing expenses, and investing consistently can significantly reduce the time required.

Advantages and Disadvantages

Like any financial strategy, this approach has both advantages and disadvantages.

Advantages

- Early retirement

- Financial independence

- More freedom and flexibility

- Less financial stress

- More control over time and lifestyle

Disadvantages

- Requires disciplined budgeting

- Lower spending lifestyle

- Investment risk

- Healthcare planning required

- Less room for unexpected expenses

This strategy works best for people who value freedom and time more than luxury spending and expensive lifestyles.

Final Thoughts

Lean FIRE is not about extreme frugality or sacrificing happiness. It is about designing a lifestyle that allows you to save more, invest more, and gain financial independence earlier in life. By controlling expenses, increasing savings, and investing consistently, early retirement becomes a realistic goal for many people.

The most important factors are spending habits, savings rate, and long‑term investing discipline. People who stay consistent and focus on long‑term goals often achieve financial independence much earlier than expected through Lean FIRE.

In the end, the goal is simple: build a life where money supports your freedom instead of controlling your time. With proper planning and smart financial decisions, early retirement can become an achievable and realistic goal rather than just a dream.