Introduction

Financial freedom is no longer just a dream for the wealthy. Today, more people are building systems that allow them to control their time, income, and lifestyle without depending entirely on a job.

So, what is a fi and why is it becoming so popular? It is a financial state where your investments and passive income cover your living expenses, allowing you to live without relying on active work. With modern tools like coast fire calculators, lean fire calculators, barista fire calculators, and fat fire calculators, achieving this goal has become more practical and data-driven.

This guide goes beyond basic definitions and gives you a complete, actionable system to understand, calculate, and achieve financial independence.

What Is a FI and How Does It Work

To clearly understand what is a fi, you need to focus on one simple concept: your money works for you instead of you working for money.

A fi is achieved when:

- Your assets generate consistent income

- Your expenses are fully covered

- You are no longer dependent on a salary

This income can come from:

- Investments

- Dividends

- Rental properties

- Online businesses

The goal is not just earning more but building sustainable income streams.

What Is a FI in Real-Life Scenarios

Many people misunderstand what is a fi because they only see it as early retirement. In reality, it is about flexibility and control.

Example:

- Annual expenses: $40,000

- Required portfolio: $1,000,000

With a 4% withdrawal rate, your investments generate enough income to sustain your lifestyle.

At this point, you:

- Can retire early

- Work part-time

- Start a business

- Travel freely

This is the practical meaning of financial independence.

What Is a FI and the Core Formula

The most common way to calculate what is a fi starts with a simple formula:

FI Number = Annual Expenses × 25

This formula is based on the 4% rule, which assumes you can withdraw 4% of your investments each year without running out of money.

However, relying only on this formula is a major mistake.

It ignores:

- Inflation

- Lifestyle changes

- Market risks

- Income diversification

That’s why advanced planning is required.

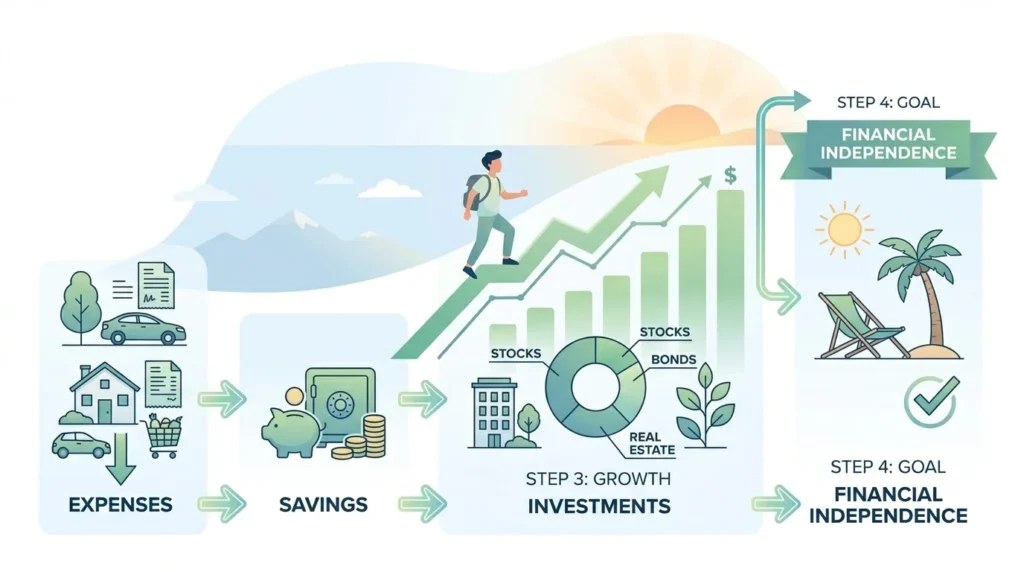

Step-by-Step System to Calculate Financial Independence

To properly understand what is a fi, follow this structured process.

Step 1: Calculate Your Annual Expenses

Track your real spending:

- Housing

- Food

- Transportation

- Healthcare

- Entertainment

Accuracy is critical here.

Step 2: Adjust for Future Lifestyle

Your expenses will change over time:

- Lower commuting costs

- Higher travel spending

- Increased healthcare expenses

Be realistic, not optimistic.

Step 3: Apply Flexible Multipliers

Instead of using only ×25:

- ×25 → standard

- ×30 → safer

- ×33 → early retirement buffer

This gives you a more reliable target.

Step 4: Factor in Inflation

Inflation reduces purchasing power.

Example:

- Today: $50,000

- In 20 years: $80,000+

Ignoring inflation leads to underestimating your target.

Step 5: Adjust for Income Streams

If you have:

- Rental income

- Dividends

- Side business

Your required investment decreases significantly.

Role of Calculators in Understanding What Is a FI

Modern financial planning depends heavily on calculators. They provide realistic projections instead of guesswork.

Coast FIRE Calculator

A coast fire calculator helps you determine how much to invest early so your portfolio grows without additional contributions later.

Lean FIRE Calculator

A lean fire calculator focuses on minimal expenses and a simple lifestyle, allowing faster financial independence.

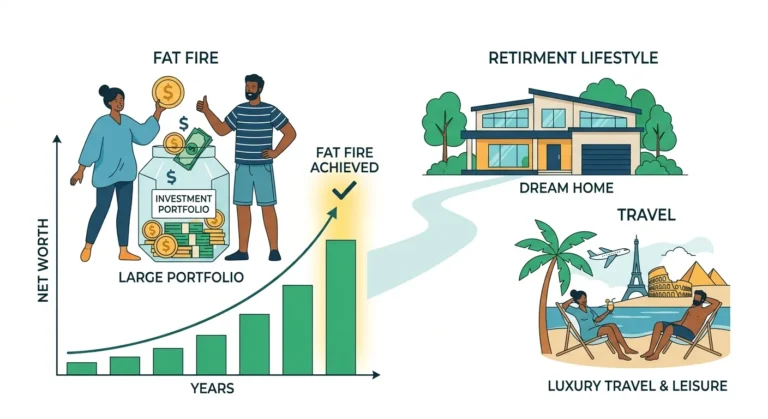

Fat FIRE Calculator

A fat fire calculator estimates a higher financial target for those who want a comfortable or luxury lifestyle.

Barista FIRE Calculator

A barista fire calculator combines part-time work with investment income, offering flexibility instead of full retirement.

Using these tools allows you to:

- Test multiple scenarios

- Plan more accurately

- Make better financial decisions

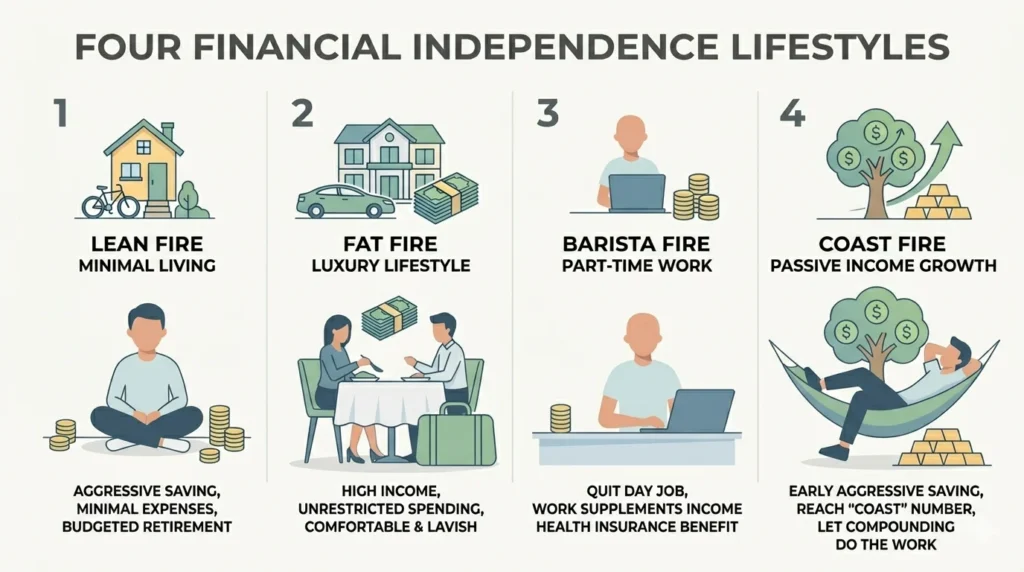

Different Types of Financial Independence

Understanding what is a fi also requires knowing its variations.

Lean FI

- Minimal expenses

- Simple lifestyle

- Faster achievement

Fat FI

- Higher spending

- Luxury lifestyle

- Larger investment goal

Barista FI

- Part-time income

- Flexible work-life balance

- Reduced financial pressure

Coast FI

- Heavy early investing

- Passive long-term growth

- Less saving required later

Comparison of FI Strategies

| Strategy | Lifestyle | Savings Needed | Speed | Flexibility |

| Lean FI | Minimal | Low | Fast | Low |

| Fat FI | Luxury | High | Slow | High |

| Barista FI | Flexible | Medium | Medium | High |

| Coast FI | Balanced | Early Focus | Long | Medium |

Key Factors That Impact Financial Independence

To fully grasp what is a fi, you must understand the core drivers.

Savings Rate

Higher savings = faster independence.

Investment Returns

Compounding significantly accelerates growth.

Expense Control

Lower expenses reduce your FI number.

Income Growth

Higher income increases your ability to invest.

Impact of Financial Decisions

| Factor | Impact Level | Control |

| Reducing Expenses | Very High | High |

| Increasing Income | High | Medium |

| Investment Returns | Medium | Low |

| Side Income | High | Medium |

This results in incomplete and unrealistic advice.

What Makes This Guide Better

This guide improves on those weaknesses by offering:

- Multiple FI models

- Step-by-step planning

- Calculator integration

- Real-life scenarios

- Risk-aware strategies

This creates a complete and practical system.

Common Mistakes to Avoid

Even with knowledge, many people fail due to mistakes:

- Underestimating expenses

- Ignoring inflation

- Overestimating returns

- Not updating plans

Avoiding these increases your success rate.

Advanced Strategies to Reach FI Faster

To accelerate your progress:

- Increase savings rate to 40–60%

- Build multiple income streams

- Invest consistently

- Use tax-efficient strategies

- Review your plan annually

Small improvements create massive long-term results.

FI vs Traditional Retirement

| Factor | FI Approach | Traditional |

| Retirement Age | Early | Late |

| Income Source | Investments | Pension |

| Flexibility | High | Low |

| Lifestyle | Self-driven | Fixed |

Real-Life Example

Scenario:

- Age: 28

- Expenses: $45,000

- Target: $1.1 million

- Monthly investment: $2,200

- Return: 8%

Estimated result:

- Financial independence in 17–19 years

Psychological Side of Financial Independence

Understanding what is a fi is not just about numbers.

It requires:

- Discipline

- Long-term thinking

- Delayed gratification

People who succeed focus on future freedom instead of short-term consumption.

Why Financial Independence Is Growing

Modern trends are accelerating this movement:

- Remote work

- Side hustles

- Online income

- Easy investing platforms

People now prioritize:

- Flexibility

- Freedom

- Control over time

Final Thoughts

Understanding what is a fi is the first step toward transforming your financial future. It is not just about money, but about creating a life where you control your time, choices, and direction.

With the right strategy, consistent investing, and smart use of calculators, financial independence becomes achievable for anyone willing to commit.

The difference between average and successful people is simple:

They don’t just learn what is a fi

They calculate it, plan it, and execute it.