How to calculate FIRE number is the first and most important step if you want to achieve financial independence and retire early. Without a clear number, you are simply guessing how much to save, invest, and plan for the future. This guide will show you exactly how to calculate your FIRE number, optimize your strategy, and use powerful tools like Coast FIRE calculator, Lean FIRE calculator, Barista FIRE calculator, and Fat FIRE calculator to speed up your journey.

What Is a FIRE Number and Why It Matters

Your FIRE number is the total amount of money you need invested so you can live off your portfolio without relying on a job. It represents financial independence.

Most people fail because they:

- Don’t define a clear target

- Underestimate expenses

- Ignore inflation and long-term risks

When you understand how to calculate FIRE number, you gain:

- Clarity and direction

- A measurable financial goal

- Better investment decisions

- Confidence in early retirement planning

How to Calculate FIRE Number (Core Formula)

The most widely used method is based on the 4% rule.

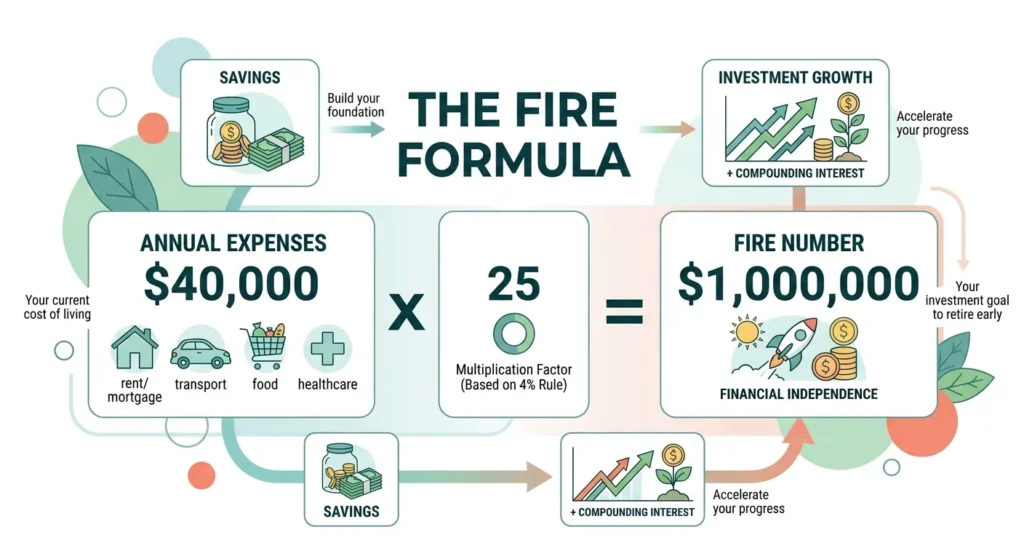

Basic Formula

FIRE Number = Annual Expenses × 25

This formula assumes you can safely withdraw 4% of your investments every year.

Example

- Annual expenses: $50,000

- FIRE number: $50,000 × 25 = $1,250,000

This means you need $1.25 million invested to sustain your lifestyle.

Understanding the 4% Rule

The 4% rule is the foundation of how to calculate FIRE number.

It suggests:

- You can withdraw 4% annually

- Your money can last 30+ years

- It adjusts for inflation

However, for early retirement, many experts recommend:

- 3% to 3.5% withdrawal rate

- Larger safety margin

- More conservative planning

Why Most Guides on How to Calculate FIRE Number Are Incomplete

Most content on how to calculate FIRE number only covers the basics, which makes it insufficient for long-term financial planning. These guides usually focus on:

- The standard formula (annual expenses × 25)

- Simple, one-size-fits-all examples

- Basic investment advice without real strategy

While this approach helps beginners understand the concept, it fails to provide the depth required to build a realistic and sustainable FIRE plan.

A More Advanced Approach to How to Calculate FIRE Number

This guide takes a complete and practical approach to how to calculate FIRE number. Instead of relying on simplified assumptions, it integrates:

- Real-world financial scenarios

- Advanced calculator-based projections

- Flexible strategies based on different FIRE models

By combining these elements, you can create a more accurate, scalable, and reliable plan for achieving financial independence.

Step-by-Step Guide on How to Calculate FIRE Number

Step 1: Calculate Your Annual Expenses

Start by tracking your actual spending:

Include:

- Housing (rent/mortgage)

- Food and groceries

- Transportation

- Healthcare

- Insurance

- Entertainment

- Travel

Avoid guessing. Use real data.

Step 2: Adjust for Retirement Lifestyle

Your future expenses may change:

- No commuting costs

- More travel expenses

- Higher healthcare costs

- Lifestyle upgrades or downsizing

Be realistic, not optimistic.

Step 3: Apply the FIRE Formula

Multiply your adjusted annual expenses by 25.

If you want extra safety:

- Use × 30 for conservative planning

- Use × 33 for early retirement

Step 4: Factor in Inflation

Inflation increases costs over time.

Example:

- Today’s expenses: $50,000

- In 20 years: could be $80,000+

Ignoring inflation leads to underestimating your FIRE number.

Step 5: Adjust for Income Streams

Reduce your FIRE number if you have:

- Rental income

- Dividends

- Side business income

- Freelancing

These reduce how much you need invested.

FIRE Number by Lifestyle (Comparison Table)

| Lifestyle Type | Annual Expenses | FIRE Number (×25) | Conservative (×30) |

| Lean Lifestyle | $30,000 | $750,000 | $900,000 |

| Moderate | $50,000 | $1,250,000 | $1,500,000 |

| Comfortable | $70,000 | $1,750,000 | $2,100,000 |

| Luxury | $100,000 | $2,500,000 | $3,000,000 |

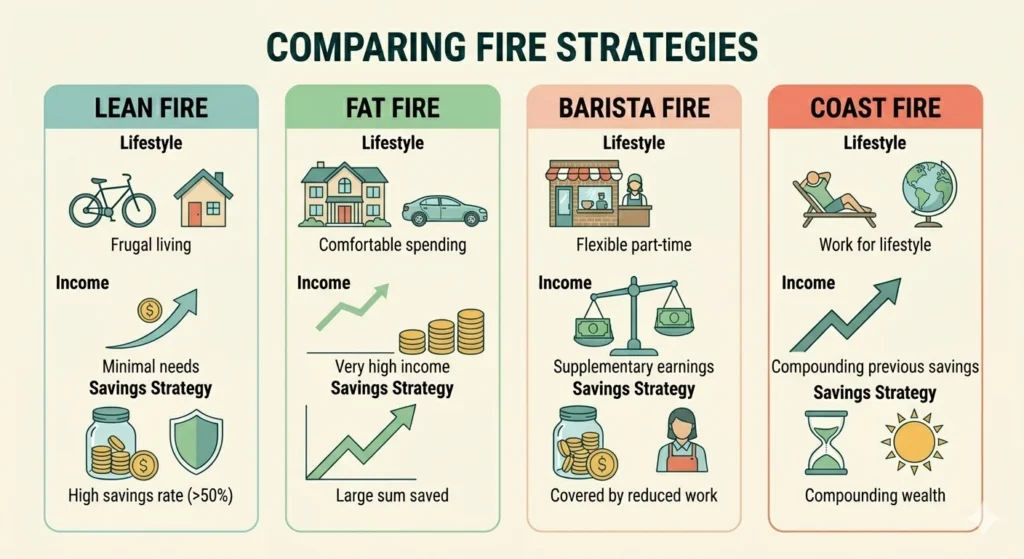

Different Types of FIRE You Must Understand

Understanding different FIRE strategies is essential when learning how to calculate your financial independence target. Each approach—coast fire, lean fire, fat fire, and barista fire—offers a unique path based on your lifestyle, income, and long-term goals.

Lean FIRE

Lean fire focuses on minimal expenses and a simple lifestyle. It is ideal for individuals who want to retire early by keeping costs low and maximizing savings. This strategy allows you to reach financial independence faster with a smaller investment target.

Fat FIRE

Fat fire is designed for those who prefer a comfortable or luxury lifestyle in retirement. It requires a larger investment portfolio to support higher spending, travel, and financial flexibility without compromising quality of life.

Barista FIRE

Barista fire combines part-time work with investment income. Instead of fully retiring, you maintain a flexible lifestyle where your savings cover part of your expenses while light work provides additional income and stability.

Coast FIRE

Coast fire focuses on investing aggressively early in life so your portfolio can grow passively over time. Once you reach a certain investment level, you no longer need heavy contributions, allowing you to reduce financial pressure later.

How to Calculate Coast FIRE Number

Coast FIRE focuses on investing early.

Formula Concept

You calculate how much you need today so it grows to your FIRE number without additional contributions.

Example:

- Target FIRE number: $1,000,000

- Invest early: $200,000

- Let compounding do the rest

This reduces long-term pressure.

Advanced Approach to How to Calculate FIRE Number Effectively

Taking an advanced approach to how to calculate FIRE number can significantly improve your financial planning accuracy. Instead of relying only on fixed formulas, you should include variables like inflation, investment returns, and changing lifestyle needs. When you apply how to calculate FIRE number with these factors, your target becomes more realistic and achievable. This approach also allows flexibility if your income or expenses change over time. By refining how to calculate FIRE number using data-driven insights, you can build a stronger, long-term strategy for achieving financial independence with confidence.

Using Calculators to Improve Accuracy

Manual calculation is not enough.

Coast FIRE Calculator

- Shows how early investments grow

- Reduces future savings pressure

Barista FIRE Calculator

- Combines part-time income with savings

- Ideal for flexible retirement

Lean FIRE Calculator

- Focuses on low-cost lifestyle

- Helps retire faster

Fat FIRE Calculator

- Calculates high-end retirement goals

- Includes luxury spending

Investment Calculator

- Projects compound growth

- Shows timeline to reach your goal

FIRE Strategy Comparison Table

| Strategy | Savings Rate | Lifestyle | Risk Level | Time to FIRE |

| Lean FIRE | High | Minimal | Low | Fast |

| Fat FIRE | Moderate | Luxury | Medium | Slow |

| Barista FIRE | Medium | Flexible | Low | Medium |

| Coast FIRE | Early Focus | Balanced | Medium | Long-term |

Key Factors That Affect Your FIRE Number

1. Lifestyle Expenses

Higher spending increases your target significantly.

2. Investment Returns

Better returns reduce required savings.

3. Inflation

Rising costs increase your FIRE number.

4. Retirement Age

Earlier retirement requires more money.

5. Income Streams

Passive income reduces your dependency on investments.

6. Risk Tolerance

Lower risk = higher required savings.

How Much Should You Save Monthly?

Once you calculate your FIRE number, the next step is:

Monthly Investment = Based on:

- Timeline

- Expected returns

- Current savings

Example:

- Target: $1,000,000

- Time: 20 years

- Return: 8%

- Monthly investment: ~$1,700

Investment Strategy for Reaching FIRE

To achieve your goal:

Focus on:

- Index funds

- ETFs

- Diversified portfolios

- Long-term compounding

Avoid:

- Speculative investments

- Overtrading

- Emotional decisions

Common Mistakes to Avoid

- Underestimating expenses

- Ignoring inflation

- Overestimating returns

- Not diversifying investments

- Setting unrealistic timelines

These mistakes delay financial independence.

Advanced Strategy: Dynamic FIRE Planning

Your FIRE number is not fixed.

It changes with:

- Career growth

- Lifestyle changes

- Economic conditions

- Family responsibilities

Review your plan annually.

How to Reduce Your FIRE Number

If your target feels too high:

- Reduce expenses

- Increase income

- Invest early

- Build passive income

- Relocate to lower-cost areas

Small changes make a big difference.

Real-Life Scenario

Person A:

- Expenses: $40,000

- FIRE number: $1,000,000

Person B:

- Expenses: $80,000

- FIRE number: $2,000,000

Same strategy, different lifestyle → double requirement.

Why Calculators Give You an Edge

Most people rely on rough estimates.

But calculators:

- Provide accurate projections

- Adjust for inflation

- Simulate multiple scenarios

- Improve decision-making

They turn planning into strategy.

Key Takeaways

- Learning how to calculate FIRE number gives you financial clarity

- The 4% rule is the foundation of FIRE planning

- Lifestyle and expenses are the biggest factors

- Different FIRE strategies change your target

- Calculators improve accuracy and speed

- Early investing is the most powerful advantage

Conclusion

Understanding how to calculate FIRE number is the foundation of financial independence. It transforms vague goals into a clear, actionable plan. While the formula is simple, true success comes from accurate planning, disciplined investing, and consistent tracking.

The biggest advantage you can have is starting early and using the right tools. By combining smart strategies with calculators and realistic assumptions, you can turn what seems like a distant goal into an achievable milestone.

Financial freedom is not about luck. It is about clarity, strategy, and consistency.