FU money is the amount of wealth that gives you the freedom to walk away from jobs, obligations, or situations without worrying about income. It represents financial independence at a personal level, where your decisions are no longer controlled by money but by your priorities and values.

In today’s fast-changing financial world, more people are shifting from traditional retirement goals toward flexible financial independence. Instead of waiting until 60 or 70, individuals now focus on building a safety net that allows them to take control much earlier. This is where FU money becomes powerful. It is not about luxury or quitting work forever—it is about having options.

This guide goes deeper than typical explanations. You will learn how to calculate it, how it compares with other financial strategies, how to build it faster, and how to use modern calculators to plan effectively.

What Is FU Money and Why It Matters

Understanding what is FU money helps you rethink how financial success is measured. Instead of focusing only on retirement, it focuses on freedom and flexibility.

Key advantages include:

- Freedom to leave a toxic job

- Ability to take career breaks

- Reduced stress about income

- Confidence in decision-making

- Flexibility to explore new opportunities

Most financial advice revolves around long-term planning, but FU money gives you immediate control over your life.

What Is FU Money Mean in Real Life

When people search what is FU money mean, they are really asking how much money is enough to feel secure.

In practical terms, fu money usually covers:

- 1 to 5 years of living expenses

- Emergency savings

- Basic lifestyle needs without active income

It is not full retirement wealth. Instead, it acts as a financial buffer that allows you to pause, pivot, or reset your life without pressure.

FU Money vs Financial Independence

Many people confuse FU money with full financial independence, but they serve different purposes.

| Aspect | FU Money | Financial Independence |

| Goal | Flexibility | Permanent freedom |

| Time Horizon | Short to mid-term | Long-term |

| Amount Needed | Lower | Higher |

| Work Dependency | Optional | Not required |

| Lifestyle | Flexible | Fully funded |

Fu money is often the first stage before achieving complete financial independence.

How to Calculate FU Money

You can estimate your target using a simple formula.

FU Money = Monthly Expenses × Desired Freedom Period

Example:

- Monthly expenses: $3,000

- Freedom period: 24 months

Required amount = $72,000

This calculation shows why FU money is more achievable than traditional retirement goals.

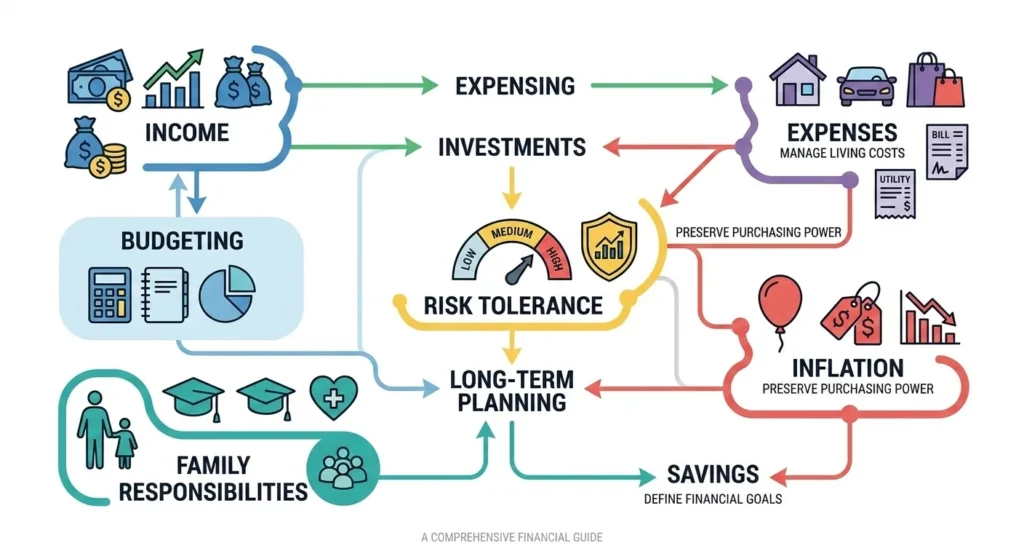

Factors That Affect Your FU Money Target

Lifestyle Expenses

Your daily living expenses are the foundation of your fu money calculation. The more you spend on housing, food, travel, and entertainment, the higher your required savings will be. Tracking your monthly expenses accurately helps you set a realistic and achievable financial target.

Risk Tolerance

Your comfort level with financial uncertainty plays a key role. If you prefer stability and low risk, you may want a larger financial cushion. On the other hand, individuals who are comfortable with risk may rely more on investments and maintain a smaller buffer.

Income Stability

Your income source directly impacts how much fu money you need. Freelancers, entrepreneurs, or individuals with irregular income typically require a larger safety net compared to those with stable, salaried jobs. A predictable income reduces the pressure on your savings.

Family Responsibilities

If you have dependents, your financial responsibilities increase significantly. Expenses such as education, healthcare, and daily living costs must be factored into your plan. The more people relying on you, the higher your financial security target should be.

Cost of Living

Your geographical location has a major impact on your financial needs. Living in a high-cost city requires significantly more savings compared to a low-cost area. Adjusting your lifestyle or relocating can dramatically reduce your required fu money target.

Inflation Impact

Inflation gradually increases the cost of living over time. Ignoring inflation can lead to underestimating your financial needs. A smart plan always accounts for rising expenses to maintain long-term purchasing power.

Investment Returns

The performance of your investments affects how quickly you reach your goal. Higher returns can reduce the amount you need to save, while lower returns may require additional contributions. Diversified investments help balance risk and growth.

Emergency Buffer

Unexpected expenses such as medical bills or job loss can disrupt your financial plan. Including an extra buffer within your FU money ensures you stay protected even during uncertain situations.

How to Build FU Money Faster

Achieving FU money requires discipline and strategy.

Increase Savings Rate

Aim to save 30 to 50 percent of your income.

Reduce Expenses

Cut unnecessary costs and avoid lifestyle inflation.

Eliminate Debt

Lower liabilities improve financial flexibility.

Invest Consistently

Focus on long-term growth assets like index funds and ETFs.

Create Multiple Income Streams

Examples include freelancing, online businesses, and rental income.

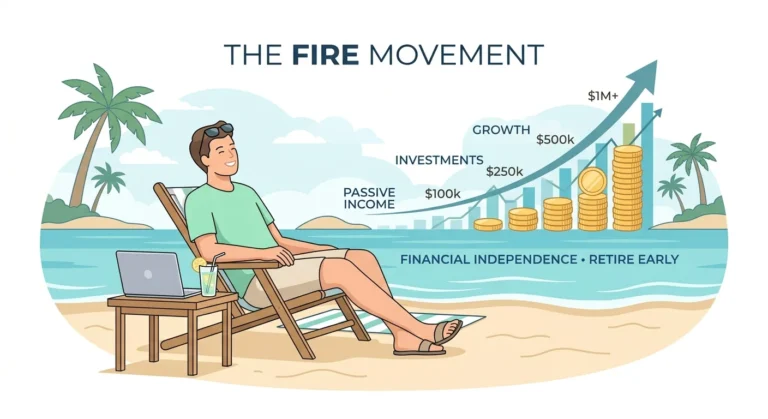

Powerful Calculators to Achieve Your Financial Goals Faster

Manual calculations can give you a rough estimate, but they often miss important variables like inflation, investment growth, and lifestyle changes. This is where financial calculators give you a clear advantage. They turn assumptions into accurate, data-driven projections and help you plan your fu money target with confidence.

Coast FIRE Calculator

A Coast FIRE Calculator helps you estimate how much you need to invest early so your portfolio can grow on its own without additional contributions. This is ideal if you want to reduce long-term savings pressure while still moving toward financial freedom.

Barista FIRE Calculator

A Barista FIRE Calculator shows how part-time income combined with your savings can support your lifestyle. It is perfect for those who want flexibility instead of full retirement, allowing you to work less while maintaining financial stability.

Lean FIRE Calculator

A Lean FIRE Calculator focuses on minimal expenses and a simple lifestyle. It helps you calculate how quickly you can reach financial independence by reducing spending and optimizing savings.

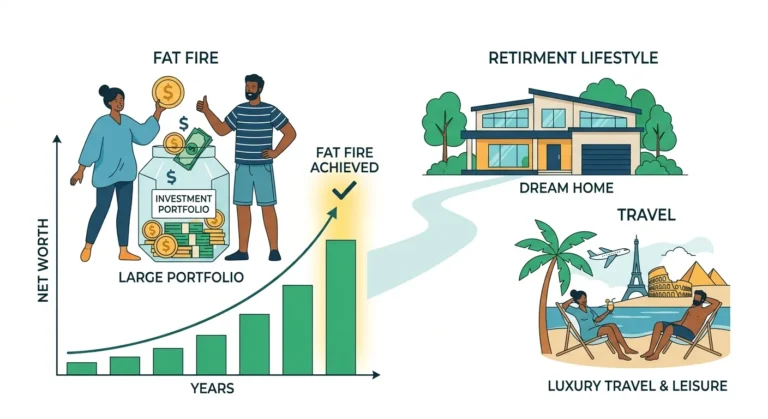

Fat FIRE Calculator

A Fat FIRE Calculator is designed for those who want a higher standard of living in retirement. It calculates a larger financial target that includes travel, luxury, and greater financial flexibility.

FU Money vs Emergency Fund

These two concepts are often confused, but they are different.

| Feature | FU Money | Emergency Fund |

| Purpose | Freedom | Protection |

| Duration | Long-term | Short-term |

| Usage | Life decisions | Emergencies |

| Impact | Empowerment | Security |

An emergency fund helps you survive. Fu money helps you take control.

Psychological Benefits of FU Money

One of the most powerful aspects of FU money is its mental impact.

Confidence

You gain the ability to make bold decisions.

Reduced Stress

Financial anxiety decreases significantly.

Career Freedom

You work by choice, not necessity.

Better Negotiation Power

You are less dependent on any single income source.

This mental shift is often more valuable than the money itself.

Common Mistakes to Avoid

Underestimating Expenses

Always include hidden costs like healthcare and inflation.

Keeping Cash Idle

Inflation reduces purchasing power over time.

Relying on One Income Source

Diversification is essential.

Setting Unrealistic Targets

Start small and scale gradually.

Ignoring Inflation

Future costs will always be higher.

Advanced Strategy: FU Money and FIRE Together

Instead of choosing one approach, combine them.

Step 1: Build FU Money

Save enough for 1 to 3 years of expenses.

Step 2: Transition to Coast FIRE

Let your investments grow while reducing workload.

Step 3: Achieve Full Financial Independence

Reach a level where work becomes optional permanently.

This hybrid strategy accelerates financial freedom while reducing risk.

Real-Life Example

Person A:

- Annual expenses: $40,000

- FU money target: $120,000

Person B:

- Annual expenses: $80,000

- FU money target: $240,000

Same strategy, but lifestyle differences double the requirement.

Why Financial Independence Is Gaining Popularity

Modern financial trends are rapidly evolving, and people are rethinking how they approach work, income, and long-term security. Traditional career paths no longer guarantee stability, which is pushing individuals to seek more control over their financial future.

Several key shifts are driving this change:

- Job security is becoming less reliable in many industries

- Remote work is opening new income opportunities

- Side hustles and multiple income streams are more common than ever

- People now prioritize flexibility, freedom, and work-life balance over long-term job stability

As a result, more individuals are focusing on building financial independence early. Instead of relying on a single income source, they are creating systems that allow them to make life decisions without financial pressure.

This approach aligns perfectly with modern lifestyles, where freedom, adaptability, and control matter more than traditional definitions of success.

Competitor Gap Analysis and Improvements

Most competitor content is limited and lacks depth. It usually focuses only on basic definitions and simple benefits.

This guide improves by including:

- Detailed calculation methods

- Strategic comparison tables

- Integration of FIRE calculators

- Step-by-step wealth-building strategy

- Advanced hybrid planning approach

- Psychological and lifestyle insights

- Real-world examples

These additions make the content more practical, actionable, and SEO-optimized.

Key Takeaways

- Fu money is a financial buffer that provides freedom and flexibility

- It is different from full financial independence

- You can calculate it based on your expenses and time horizon

- Financial calculators improve accuracy and planning

- Combining fu money with FIRE strategies accelerates results

- The biggest benefit is control over your life decisions

Final Thoughts

Understanding what is FU money can transform your financial strategy completely. It shifts your focus from distant retirement goals to immediate freedom and flexibility. You do not need millions to achieve it. With the right plan, disciplined saving, and smart investing, you can build a financial cushion that gives you control over your life.

Start early, stay consistent, and use tools like calculators to guide your progress. Once you reach your target, you will realize that FU money is not just about wealth—it is about living life on your own terms.